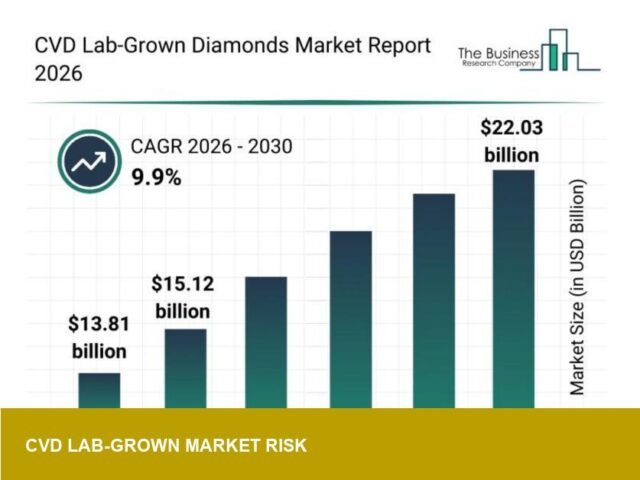

The Business Research Company has released a market report, published on openPR.com, titled “Key Factors and Emerging Trends Shaping the CVD Lab-Grown Diamonds Market Landscape.” The analysis frames the commercial dynamics around chemically vapor‑deposited (CVD) lab‑grown diamonds and flags implications for retail margins, inventory strategy and distribution channels in the US jewellery market.

- Publisher: The Business Research Company

- Distribution: openPR.com (press release)

- Subject: CVD lab‑grown diamonds (chemical vapor deposition)

- Primary audience: retailers, wholesalers and investors assessing margin and inventory risk

Context: where CVD fits in current jewellery trends

The report’s framing places CVD lab‑grown diamonds at the intersection of three industry pressures: production scale, trade‑channel acceptance and consumer positioning. CVD as a production method now delivers stones with consistent proportions across cut, colour and clarity grades, narrowing aesthetic differences that once separated lab‑grown and mined goods. That technical parity shifts commercial conversations away from novelty and toward assortment strategy — how much of a bridal or fashion assortment should carry lab‑grown SKUs versus natural diamonds, and at what price spread.

Traceability and sustainability remain touchpoints in the narrative. Retail buyers are increasingly treating origin disclosure and recycled metals as table stakes; CVD product positioning often leans on lower environmental footprint and controlled provenance. Those claims influence marketing copy and certificate expectations rather than intrinsic gemology — retailers must therefore be fluent in the language of sustainability claims and in documented chain‑of‑custody to avoid margin leakage on post‑sale remediation.

Impact: what US retailers, wholesalers and investors should do

For US retailers the report sharpens a few operational imperatives. Merchants should reassess inventory velocity and margin profiles on lab‑grown lines: visual parity and lower landed cost for CVD goods can compress retail margins on comparable mined SKUs unless assortments are differentiated by setting, craft and service. Consider emphasising tangible craft distinctions — knife‑edge shanks, open‑backed settings for light performance, micro‑pavé execution — that preserve perceived value even when the centre stone is lab‑grown.

Wholesalers and online platforms will need clearer merchandising rules and certificate protocols. Standardise grading and provenance documentation for CVD inventories, and align return and warranty policies to avoid post‑purchase disputes that erode margins. For investors and category buyers, the report suggests reweighting forecasts to reflect supply predictability from CVD manufacturing and potential channel migration away from older, higher‑cost mined inventory.

Ultimately, the report underlines that CVD lab‑grown diamonds are no longer a fringe product for a niche buyer. Their commercialisation forces pragmatic choices: tighter assortment segmentation, firmer certificate standards, and disciplined price architecture to protect margins while responding to growing consumer acceptance.

Image Referance: https://www.openpr.com/news/4428149/key-factors-and-emerging-trends-shaping-the-cvd-lab-grown